Q3'16 Micro Cap Value Strategy

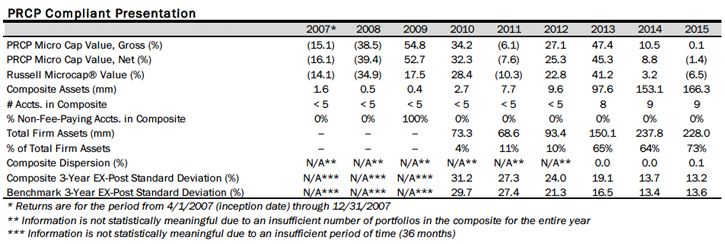

The Pacific Ridge Capital Partners (“PRCP”) Micro Cap Value strategy returned 14.6% for the third quarter of 2016, ahead of the 10.8% return for the Russell Microcap© Value Index (“Index”). Over the trailing one-, three-, and five-year periods, the strategy returned 26.2%*, 12.6%*, and 23.6%* (annualized), respectively, compared to the Index returns of 15.7%, 6.2%, and 16.5%. Since inception on April 1, 2007, the strategy has returned

10.1%* annually versus 3.8% for the Index.

The third quarter began with equity markets continuing their recovery from the sell-off that followed the Brexit vote in late June. The quarter concluded with two of the world’s largest banks facing intense scrutiny, though for different reasons. In Germany, Deutsche Bank (“DB”) has seen its stock price falter as questions have been raised about their capital adequacy and the potential need for a bailout. This concern was amplified upon news reports that some hedge fund clients had begun reducing their cash exposure as the bank worked to secure a multi-billion-dollar settlement with the US government relating to improper packaging of mortgage backed securities. Closer to home, Wells Fargo (“WFC”) has been under heavy scrutiny following revelations that pressure from management to meet internal sales targets led to millions of accounts being opened for customers without their authorization. While both banks will likely weather the current storm, they have much work to do on the public relations front. However, just as Brexit has faded from the headlines, assuming DB reaches a settlement and WFC makes a few internal changes, we anticipate these news stories will fade as well. With an election looming next month and the Federal Reserve potentially making news in December, investors will quickly shift their focus.

The Micro Cap Value strategy experienced a moderate tailwind due to size bias this quarter. Approximately 90% of the strategy’s holdings were under $400 million in market capitalization, versus 57% for the Russell Microcap Value. This smaller end of the Index actually outperformed the broader Index, 12.7% vs. 10.8%. From a sector standpoint, strong stock selection in Materials and Information Technology added over 180 basis points to the strategy’s excess return. However, poor stock selection in Health Care detracted almost 200 basis points of return versus the Index. In addition, the lack of Real Estate and Utilities holdings in the strategy (the two worst-performing sectors in the Index with returns of +5.5% and -0.7% and weights of 8.0% and 1.8%, respectively) accounted for about a 60 basis points tailwind for us during the quarter.

Industrials remained the highest weighted sector in the strategy at 28.8%. This is also the greatest overweight sector compared to the Index at 12.1%. The strategy’s holdings in the sector rose 13.0% in the period, compared to a 10.0% gain in the Index. The greatest contributor to performance in the sector was Acacia Research (“ACTG”), with its shares returning 48.2% in the quarter. ACTG, a licensor and enforcer of technology patents, reported quarterly earnings which were well ahead of estimates as the Company continues its turnaround and looks to expand its intellectual property portfolio. New management has done a good job of cutting expenses, shifting their focus to smaller deals, and maintaining a large cash position.

Manitex (“MNTX”), a designer and manufacturer of cranes and boom trucks, was the greatest detractor to returns in the Industrials sector, with the shares down 20.5% in the quarter. This industry has been choppy as demand from the energy industry has been subdued. Management is addressing this through cost reductions and divestitures of lower margin product lines to stabilize profits and improve its balance sheet. Having survived one previous down cycle, MNTX is well positioned for a recovery in its more diversified end markets.

Financials was the second highest weighted sector in the strategy at 25.8%. This was the greatest underweight compared to the Index at 35.3%. It is important to note that Real Estate is no longer included within the Financials sector. This is the first quarter it has been broken out as a separate sector and its weights and returns are no longer calculated within Financials. The strategy’s holdings in Financials increased 11.4% during the period, compared to a 10.9% gain in the Index. The greatest contributor to sector performance was People’s Utah Bancorp (“PUB”), a Utah based community bank. PUB reported better than expected Q2’16 results, which resulted in a 23.1% return for the quarter. The bank is currently sitting on a large amount of excess capital and generates a top decile return on capital compared to other US banks. Additionally, PUB is realizing above-average loan growth and continues to trade at a slight discount to what we consider as fair value.

Northrim Bancorp (“NRIM”) was the greatest detractor to returns in the Financials sector for the quarter, despite its shares being down only 1.3% during the period. NRIM is an Anchorage, Alaska-based community bank, with additional branches in Fairbanks, Sitka, and Juneau. There are very few community banks in their markets, therefore, competition is limited to First National Bank of Alaska, Wells Fargo, KeyCorp, and various credit unions. The favorable environment has led to solid net interest margins and high returns on equity, though they have recently seen a slight deterioration in credit. If NRIM can manage through this credit issue and continue to generate profits from their mortgage origination business, we feel the stock should increase in value.

Information Technology was the third highest weighted sector at 22.7%, compared to 11.2% in the Index. The strategy’s holdings in this sector rose 25.0% during the period, compared to a 16.3% gain in the Index. PCM (“PCMI”), a seller of technology products, services and solutions, was the greatest contributor to returns in the sector, with shares up 93.4% during the quarter. PCMI reported earnings in late July that came in well ahead of estimates, as they experienced strong growth in higher margin software sales. Recent acquisitions have led to improved scale and operating leverage, which is further boosting margins. The stock continued its rally post-earnings, and has recently moved into the low-$20s. Despite the big move in its shares, we believe there is nice upside as the Company continues to move toward the operating margin level of its peers.

Amtech Systems (“ASYS”) was the greatest detractor to returns in the Information Technology sector, with its shares down 16.9% for the quarter. ASYS, a manufacturer of capital equipment used in the fabrication of solar cells, LED and semiconductor devices, saw their stock weaken recently as the capital spending cycle in the solar industry has been in the early stages of recovery. This cycle is driven by the replacement of the current installed base with higher efficiency cell architectures. With indications that the back half of the year may see an uptick in orders, the stock could perform well as ASYS generates operating leverage from their underutilized capacity.

As always, we continue to search for companies that demonstrate an ability to earn a fair return on capital. We welcome any questions or comments you may have, and thank you for your continued support.

Sincerely,

Pacific Ridge Capital Partners

*Returns are preliminary

Note - sector weights for the strategy and index are the average for the period

Disclosures

Pacific Ridge Capital Partners, LLC (“Pacific Ridge”, “PRCP”, or “the Firm”) is a 100% employee owned investment advisor registered with the Securities and Exchange Commission under the Investment Advisors Act of 1940. The Firm was established in June 2010, and has one office located in Lake Oswego, Oregon. Pacific Ridge claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. PRCP has been independently verified for the periods June 10, 2010 through June 30, 2016. Verification assesses whether (1) the Firm has complied with all the composite construction requirements of the GIPS standards on a firm-wide basis and (2) the Firm’s policies and procedures are designed to calculate and present performance in compliance with the GIPS standards. The Micro Cap Value composite has been examined for the periods June 10, 2010 through June 30, 2016. The verification and performance examination reports are available upon request.

The Micro Cap Value composite was created on June 10, 2010. The Micro Cap Value composite comprises fully discretionary portfolios managed by the Firm invested primarily in a concentrated equity portfolio of smaller companies with market capitalizations similar to those found in the Russell Microcap® Index. The strategy ascribes to a disciplined bottom-up fundamental selection process with an emphasis given to the cash flow generating capabilities of a company. The strategy’s objective is to outperform the Russell Microcap® Value Index which is used as our benchmark. Eligible portfolios must be managed for a full calendar month prior to inclusion in the Micro Cap Value composite. Prior to June 10, 2010 the performance represents the track record established by the Portfolio Management Team while affiliated with prior firms. The portability of the prior track record has been reviewed by Ashland Partners & Company LLP. Composite dispersion is measured using an asset weighted standard deviation of returns of the portfolios. Returns and asset values are stated in US dollars.

The Russell Microcap® Value Index measures the performance of the microcap segment of the U.S. equity market. For comparison purposes, the index is fully invested, which includes the reinvestment of income. The return for the index does not include any transaction costs, management fees or other costs.

Sources: Pacific Ridge; FactSet Research Systems (“FactSet”); and Russell Investment Group (“Russell”) who is the source and owner of the Russell Index data.

Returns for the Micro Cap Value composite are presented gross and net of management fees and other expenses and includes realized and unrealized gains and losses, cash and cash equivalents and related interest income, and accrued based dividends. Net returns are calculated by deducting the highest annual management fee of 1.50% from the quarterly gross composite return. All returns are calculated after the deduction of the actual trading expenses incurred during the period.

The management fee is a flat rate of 1.50%.

The portfolio characteristics, sector weightings and attribution analysis for the Micro Cap Value composite are based on a representative account within the strategy. The representative account statistics are shown as supplemental information. The Firm maintains a complete list and description of composites, policies for valuing portfolios, calculating performance, and preparing compliant presentations which are available upon request by contacting Peter Trumbo, Chief Compliance Officer at (503) 886-8972 or Peter.Trumbo@PacificRidgeCapital.com.

Top 5 and Bottom 5 Performing Securities represent those security holdings that had the largest positive and negative total contribution to the portfolio return. Top 3 and Bottom 3 Economic Sectors represent those sectors that had the largest positive and negative total contribution to the portfolio return.

In order to maintain consistency when comparing the Micro Cap Value strategy to the Russell benchmark, the Firm utilizes FactSet’s outlier methodology calculations which provide a comparable portfolio characteristic calculation methodology as Russell applies to its indices.

The information provided should not be considered a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in our strategy at the time you receive this report or that securities sold have not been repurchased. It should not be assumed that any of the holdings discussed herein were or will be profitable or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein. Past performance is no guarantee of future results.

Although the statements of fact and data in this report have been obtained from, and are based upon, sources that the Firm believes to be reliable, we do not guarantee their accuracy, and any such information may be incomplete or condensed. All opinions included in this report constitute the Firm’s judgment as of the date of this report and are subject to change without notice. This report is for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security.