Investment Philosophy

During many of our conversations with clients, we are asked about the kinds of companies that we like to buy and how we find them. In our letter to you from April 2011, we outlined the broad concept of identifying good companies trading at low prices. In this letter, we share with you the three categories these companies fit into, and at what point in the economic cycle one group is more prevalent than others.

Oversold. Companies in this category tend to proliferate in periods of high volatility or near the end of an economic cycle. Many happen to have cash-rich balance sheets from recently completed IPO's. During good times, these companies are bid up to unreasonable highs. Investors who push these prices up to such levels often times have itchy trigger fingers, and they will look to exit at the first sign of a slowdown in projected growth rates. The typical sell-off is generated by an earnings announcement that does not meet analyst expectations – the dreaded "earnings miss." As more and more stock gets dumped on the market, the price continues to fall and overshoot what would be a reasonable valuation with the new information. What distinguishes these stocks is their parabolic price decline over a matter of days. Oversold companies are often accompanied by new highs in the markets, or (by definition) periods of high volatility, much like we have seen in the last few years.

Neglected Stocks. Companies that have limited Wall Street analyst coverage and lower institutional ownership are the bread and butter of low price stock pickers like us. Companies that fit into this category are found in all industries, and are not displaying the high growth profiles of other faster growing companies. This creates limited interest in these wallflower businesses. However, if you can find a neglected company generating at least average returns with benign financial risk, the market will eventually recognize its good operating performance and bid the stock up. There is always a reckoning in the market for stocks, and investors are on a continual search for good operators. Neglected companies usually don't stay that way forever, unless there is some structural impediment to their case, such as a recalcitrant management team or dual class ownership. Generally, however, these are just companies that are plodding along making reasonable returns; a classic "tortoise and the hare" scenario. Neglected companies exist in all market cycles, but tend to become more prevalent following a strong IPO market, as investors hop, skip, and jump from one "hot story" to the next.

Earnings Turnarounds. An earnings turnaround situation is most prevalent in the early stages of an economic recovery. There are three basic kinds of turnaround opportunities: Sales Turnaround, Cost Restructuring, or Balance Sheet Restructuring. In our experience, the most difficult situation is a sales turnaround, as many times a major decline in sales signals an erosion in the value proposition being brought to a company's customers. Cost and balance sheet restructurings tend to offer the most upside, and the earnings leverage can be very high. In the case of a balance sheet restructuring, the creditors of a company can be persuaded to revalue their security in the firm (at great expense to the existing shareholders) and thereby remove much of the financial risk for new shareholders (us). In other cases, a company may need a lengthy period of restructuring its operations in order to return to profitability. In all cases we look for some asset value, or minimum cash flow, that will allow the company to weather the period of transition.

These categories are not exclusive, nor do they completely encapsulate our investment strategy. We look for companies that can generate an inflation-adjusted return on their capital, and we look to pay a low price for that. Different cycles in the economy often present us with different kinds of companies to buy that can meet our criteria. We buy what is cheap and sell what is dear.

Practicing this contrarian style not only requires a strong stomach, but an ability to ignore what the popular sentiments are. It cannot tolerate the impatience of a short horizon. Not every investor has the ability to wait, and not every investment firm is designed for this pursuit. Ours is—and we look forward to discussing this more with you in the coming year.

Sincerely,

Pacific Ridge Capital Partners

About Pacific Ridge Capital Partners

Pacific Ridge Capital Partners is an employee-owned firm. We generate our own investment ideas using fundamental analysis and bottom-up stock picking. The investment team applies a consistent, patient and disciplined process that results in low turnover and stability. Our proven philosophy has performed well over many investment cycles and it is the consistent application of this strategy that makes Pacific Ridge unique.

The principals of Pacific Ridge Capital Partners are invested along with our clients in each of our strategies.

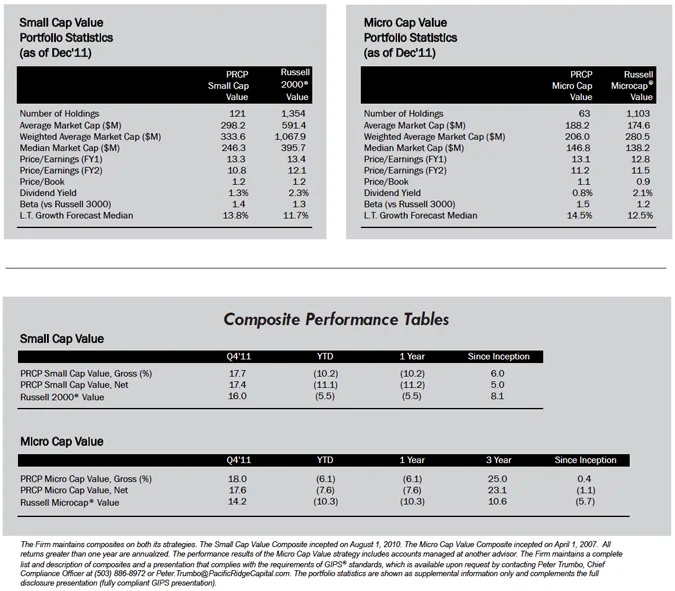

PRCP Small Cap Value – Our Small Cap Value strategy generally purchases stocks in the bottom three-quarters of the Russell 2000® Index. This smaller capitalization segment has a large number of underfollowed companies, providing us the greatest opportunity to exploit market inefficiencies. The typical range of holdings is between 100 and 150.

PRCP Micro Cap Value – Our Micro Cap Value strategy generally purchases stocks in the Russell Microcap® Index. This segment is widely underfollowed, providing us the greatest opportunity to exploit market inefficiencies. The typical range of holdings is between 50 and 80.

We believe these market cap segments offer great potential returns and additional diversification for our clients. For further information about Pacific Ridge Capital Partners and our investment strategies, we invite you to contact Tammy Wood via email at Tammy.Wood@PacificRidgeCapital.com or by phone at (503) 878-8502.

Disclosures

Pacific Ridge Capital Partners, LLC (“Pacific Ridge”, “PRCP”, or “the Firm”) is an employee-owned investment advisor registered with the Securities and Exchange Commission under the Investment Advisor Act of 1940. The Firm was established in June 2010, and has one office located in Lake Oswego, Oregon. Pacific Ridge claims compliance with the Global Investment Performance Standards (GIPS®).

Sources: Pacific Ridge; FactSet Research Systems (“FactSet”); and Russell Investment Group (“Russell”) who is the source and owner of the Russell Index data.

The current annual investment advisory fees for the portfolios managed in the Firm’s Small and Micro Cap Value strategies are 1.00% and 1.50% of assets, respectively. Returns for the composites are presented gross and net of management fees and other expenses and includes realized and unrealized gains and losses, cash and cash equivalents and related interest income, and accrued based dividends. The Firm calculates time weighted rates of return by geometrically linking portfolio simple rates of return at least monthly, with adjustments made for significant external cash flows. The composite returns are calculated by asset weighting the individual portfolio returns using beginning of the period values. All returns are calculated after the deduction of the actual trading expenses incurred during the period.

The information provided should not be considered a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in our strategy at the time you receive this report or that securities sold have not been repurchased. It should not be assumed that any of the holdings discussed herein were or will be profitable or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein. Past performance is no guarantee of future results.

Although the statements of fact and data in this report have been obtained from, and are based upon, sources that the Firm believes to be reliable, we do not guarantee their accuracy, and any such information may be incomplete or condensed. All opinions included in this report constitute the Firm’s judgment as of the date of this report and are subject to change without notice. This report is for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security.

The Russell 2000® Value Index measures the performance of the Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. For comparison purposes, the index is fully invested, which includes the reinvestment of income. The return for the index does not include any transaction costs, management fees or other costs.

The Russell Microcap® Value Index measures the performance of the microcap segment of the U.S. equity market. For comparison purposes, the index is fully invested, which includes the reinvestment of income. The return for the index does not include any transaction costs, management fees or other costs.

Returns and asset values are stated in US dollars.