Cotton Kings and Fraidy Cats

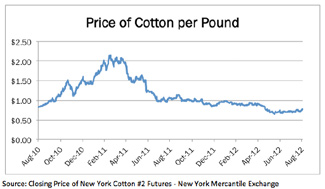

In our letter of January 2011, we highlighted how a transitory supply disruption of cotton had caused a price spike for the commodity. Well, sure enough, as the higher prices attracted larger plantings of cotton worldwide, the price has plummeted.

In 2008/2009, the consumption of cotton dropped 11%, creating an unusually high "stocks/use" ratio (nearly 65%, a 30 year record). Looking at these numbers, farmers naturally cut back on plantings for the following year. According to the U.S. Department of Agriculture, worldwide cotton production fell 5% in 2009/2010 as planters braced for the reduced demand anticipated by a continuing recession. However, smack in the middle of that production year, the spot price of cotton began to climb from $0.82 per pound to $2.15 per pound. So what happened? Worldwide consumption of cotton rebounded in early 2010, unexpectedly rising 8%. Reserves were drawn down and demand far outstripped all available supplies.

What do you think would be the response of cotton producers to that price increase? Consider that it costs somewhere around $0.60 to $0.70 per pound in operating costs to produce cotton. Sure enough, worldwide production of cotton grew 22% over the ensuing two years. Unfortunately, during that same period, consumption dropped nearly 11%. The result has been excess supply and the current price of cotton has dropped to $0.73 per pound. Although production in the U.S. has been moderated, China, India, Pakistan, and even Brazil have been adding to stockpiles.

The data is the data. However, it's difficult to make money on just data, unless you have it before everyone else. For us as investors, it is the unique insights that we bring to the interpretation of the data that matters. Is the price of cotton influenced more by the strength of the dollar or stockpiles of cotton reserves in China? Is it the introduction of cheaper synthetic fibers or is it the proliferation of boll weevils? Are financial speculators the cause of a price spike? These insights and their interpretation create opposing views, which in turn creates buyers and sellers; that is demand and supply.

Sometimes, investors forget that basic supply and demand is what drives prices of all goods and assets (at least those that operate in a free market). During the last several years, there has been quite a bit of discussion about the demand for stocks and bonds. We thought it would be a good idea to look at a few of the numbers and see what we can decipher.

The first place we look is at the mutual fund and ETF data. It's a good sample, representing over $13 trillion, according to the Investment Company Institute. Fund flow data gives us a good indication of where investors are looking to invest. Recent fund flow data indicates that since May 2007, investors have been favoring bonds over equities. The trend has been quite clear since 2008, with dollars flowing out from equity and money market funds and moving into bond funds. The simple answer is that demand for equity and money market funds has been decreasing and demand for bonds has been rising. One might expect that as demand has increased, supply would adjust and new prices would be established.

On the contrary, supply is barely keeping up with demand, forcing yields down. The obvious indicators are the rates on sovereign debt of stable countries. Strangely, in some cases, investors are paying these sovereigns for the privilege of lending to them. Fear of loss can be the only justification for this.

This trend is not just limited to the sovereign debt. Issuers of high quality corporate credits are getting rates at an all time low. A recent article in the Wall Street Journal highlighted that corporate issuance is on track to have record years in terms of volume and rate. One CFO was quoted as saying, "When you have that opportunity, you go."

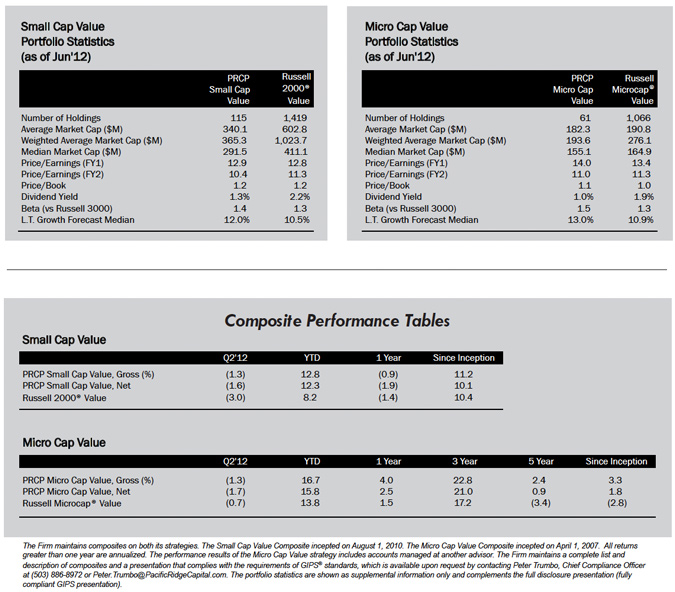

What does all of this have to do with Pacific Ridge Capital Partners, and you, our clients? Investors in small public companies are a unique breed. According to eVestment Alliance, the total amount of assets invested in "small cap value" and "micro cap value" funds is only about 3.5% of the total amount invested in U.S. equities. Additionally, search activity and new placements in the smaller asset classes is virtually non-existent. Slowing earnings growth in small companies has helped to create a dark cloud over investor's heads.

The point is that at this time, demand for domestic equities (and small cap equities in particular) is very low. The reasons are many and varied, with risk aversion likely one of the strongest factors. It is our view, however, that this will not persist forever. In fact, the U.S. equity markets will likely rise and be led by smaller companies when confidence in the future returns. As that confidence builds, demand will increase and prices will rise. Current pessimism sows the seeds of future reward.

Sincerely,

Pacific Ridge Capital Partners

About Pacific Ridge Capital Partners

Pacific Ridge Capital Partners is an employee-owned firm. We generate our own investment ideas using fundamental analysis and bottom-up stock picking. The investment team applies a consistent, patient and disciplined process that results in low turnover and stability. Our proven philosophy has performed well over many investment cycles and it is the consistent application of this strategy that makes Pacific Ridge unique.

The principals of Pacific Ridge Capital Partners are invested along with our clients in each of our strategies.

PRCP Small Cap Value – Our Small Cap Value strategy generally purchases stocks in the bottom three-quarters of the Russell 2000® Index. This smaller capitalization segment has a large number of underfollowed companies, providing us the greatest opportunity to exploit market inefficiencies. The typical range of holdings is between 100 and 150.

PRCP Micro Cap Value – Our Micro Cap Value strategy generally purchases stocks in the Russell Microcap® Index. This segment is widely underfollowed, providing us the greatest opportunity to exploit market inefficiencies. The typical range of holdings is between 50 and 80.

We believe these market cap segments offer great potential returns and additional diversification for our clients. For further information about Pacific Ridge Capital Partners and our investment strat- egies, we invite you to contact Tammy Wood via email at Tammy.Wood@PacificRidgeCapital.com or by phone at (503) 878-8502.

Disclosures

Pacific Ridge Capital Partners, LLC (“Pacific Ridge”, “PRCP”, or “the Firm”) is an employee-owned investment advisor registered with the Securities and Exchange Commission under the Investment Advisor Act of 1940. The Firm was established in June 2010, and has one office located in Lake Oswego, Oregon. Pacific Ridge claims compliance with the Global Investment Performance Standards (GIPS®).

Sources: Pacific Ridge; FactSet Research Systems (“FactSet”); and Russell Investment Group (“Russell”) who is the source and owner of the Russell Index data.

The current annual investment advisory fees for the portfolios managed in the Firm’s Small and Micro Cap Value strategies are 1.00% and 1.50% of assets, respectively. Returns for the composites are presented gross and net of management fees and other expenses and includes realized and unrealized gains and losses, cash and cash equivalents and related interest income, and accrued based dividends. The Firm calculates time weighted rates of return by geometrically linking portfolio simple rates of return at least monthly, with adjustments made for significant external cash flows. The composite returns are calculated by asset weighting the individual portfolio returns using beginning of the period values. All returns are calculated after the deduction of the actual trading expenses incurred during the period.

The information provided should not be considered a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in our strategy at the time you receive this report or that securities sold have not been repurchased. It should not be assumed that any of the holdings discussed herein were or will be profitable or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein. Past performance is no guarantee of future results.

Although the statements of fact and data in this report have been obtained from, and are based upon, sources that the Firm believes to be reliable, we do not guarantee their accuracy, and any such information may be incomplete or condensed. All opinions included in this report constitute the Firm’s judgment as of the date of this report and are subject to change without notice. This report is for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security.

The Russell 2000® Value Index measures the performance of the Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. For comparison purposes, the index is fully invested, which includes the reinvestment of income. The return for the index does not include any transaction costs, management fees or other costs.

The Russell Microcap® Value Index measures the performance of the microcap segment of the U.S. equity market. For comparison purposes, the index is fully invested, which includes the reinvestment of income. The return for the index does not include any transaction costs, management fees or other costs.

Returns and asset values are stated in US dollars.